The Best Way to Handle Payments at Your Tennis or Pickleball Club

May 27, 2025

Most tennis and pickleball clubs handle hundreds — if not thousands — of monthly transactions across memberships, lessons, events, retail sales, and more. With so much revenue on the line, how you accept and manage payments has a direct impact on your club’s ability to grow, serve players, and stay financially healthy.

If your current process still involves chasing down checks, juggling payment apps, or manually entering transactions into spreadsheets, it’s likely costing you more than just time.

Today’s racquet sports clubs don’t just need a way to collect payments — you need a system built to manage the real-world complexity of modern club operations. That’s where payment processors come in.

A business-grade payment processor isn’t just about moving money. It powers fast, secure, and automated transactions that keep your club running smoothly and professionally.

But what exactly is a payment processor — and why does it matter so much for tennis and pickleball clubs? We break it down below.

The role of payment processors at tennis & pickleball clubs

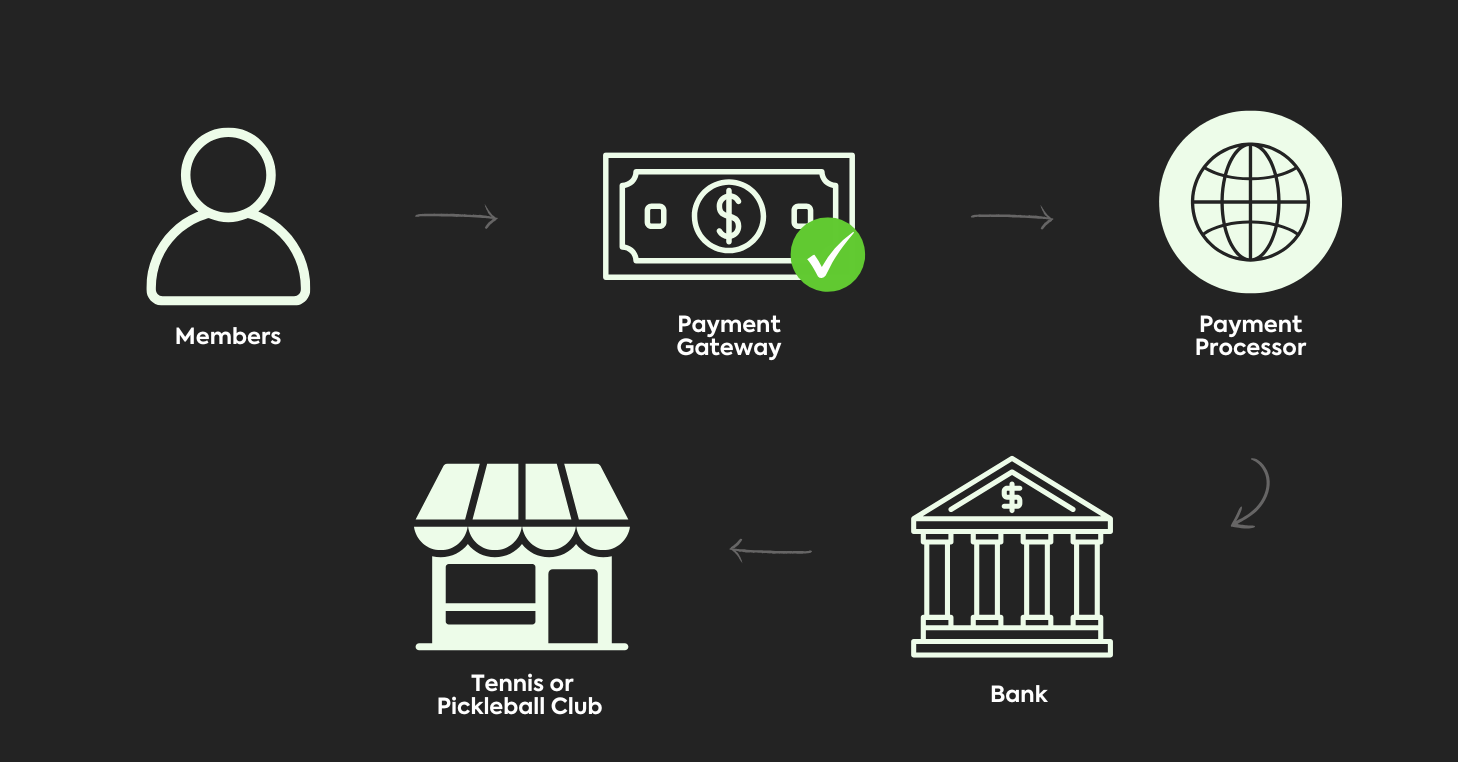

Payment processors are the behind-the-scenes technology that securely handles the movement of funds between your member’s payment method — like a credit card or bank account — and your club’s bank account.

It manages the authorization, communication, and settlement of each transaction, often in a matter of seconds. So when someone pays for a service at your tennis or pickleball club, the payment processor makes sure the money gets to you quickly, safely, and reliably.

And, modern processors do much more than just move money. They can:

Integrate with your club management platform to track payments alongside reservations and registrations

Secure sensitive data through encryption and PCI compliance

Support multiple payment methods like credit cards, ACH transfers, and even saved default payment methods for faster, more convenient checkouts

Additionally, payment processors are often paired with a payment gateway, which securely collects and encrypts payment details at checkout. Together, the gateway and processor ensure transactions are fast, secure, and successful — without requiring any manual handling by your staff.

Now, you might be thinking, “Can’t I just use PayPal or Venmo?” While those platforms work for quick, one-off payments, they aren’t built to handle the ongoing operational demands of a growing tennis or pickleball club. We’ll dive deeper into why later — for now, just know that a business-grade payment processor gives you more control, more protection, and more efficiency.

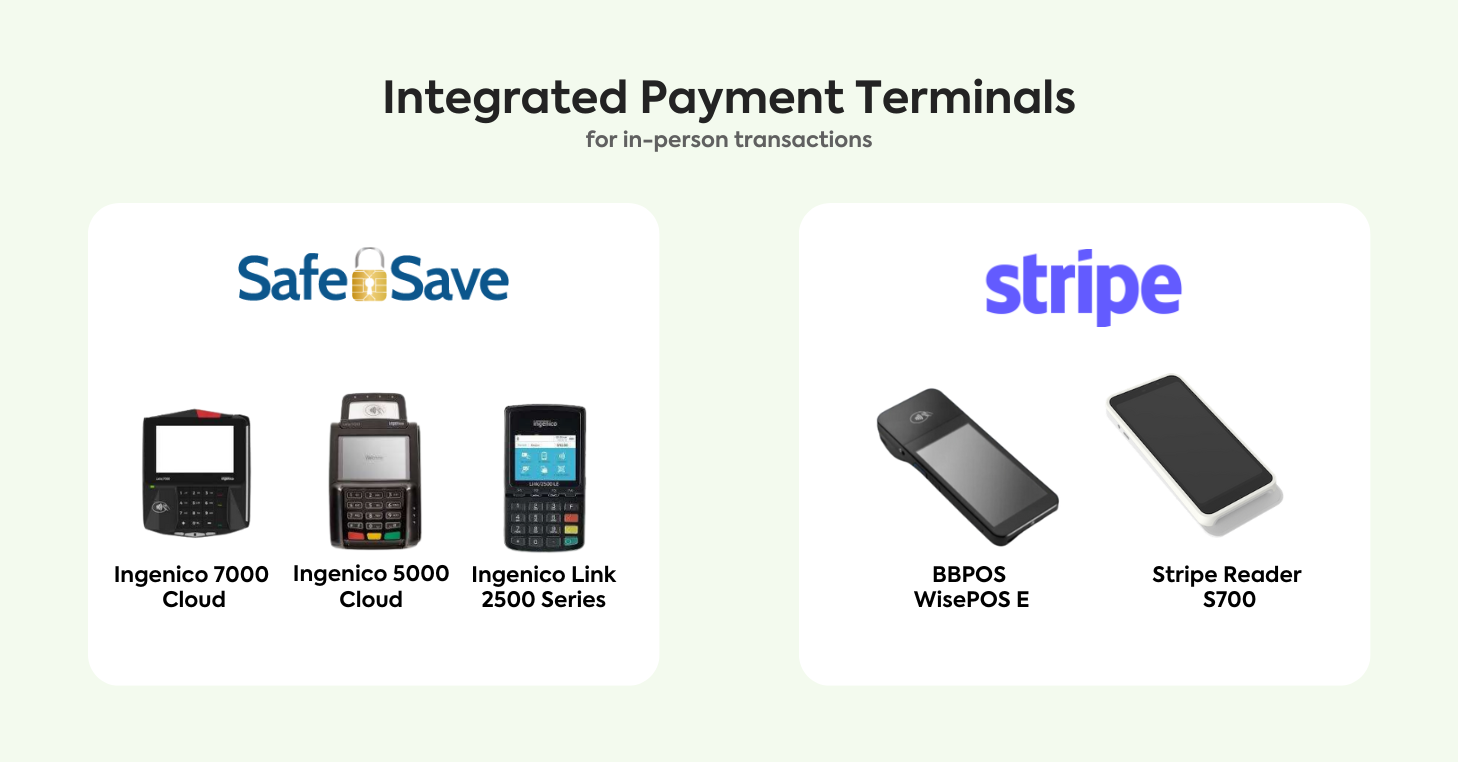

Taking digital and in-person payments

Your players expect flexibility. Some players prefer to pay in-app. Others want to swipe their card at the front desk. With an integrated payment processor, your club can accept both digital payments (via mobile app or website) and in-person transactions using physical terminals.

And because all payments run through the same system, there’s no disconnect. Every transaction — online or on-site — is securely processed and automatically linked to the correct member, booking, or purchase inside your club management platform.

That means fewer errors, faster checkouts, and less manual work for your staff. It’s one payment system that keeps everything (and everyone) in sync.

But what about transaction fees?

We get it — transaction fees can feel like a barrier. For many clubs, it’s the reason they hesitate to adopt a payment processor. Why pay to get paid, right?

Here’s the bigger picture: those fees are an investment in time savings, accuracy, and peace of mind.

When you factor in time spent chasing down late payments, dealing with bounced checks, manually updating spreadsheets, and correcting entry errors, the real cost becomes clear — and it often far exceeds the small percentage taken by a processor. Plus, a reliable payment processor helps smooth out your cash flow, ensuring payments are deposited automatically and consistently.

Yes, you’ll pay a small fee per transaction — but you’ll also save time, reduce risk, and improve billing consistency across your business, meaning it pays for itself many times over.

So, you’re not just paying for a service — you’re investing in a smarter, more stable way to run your club.

Why do clubs need a payment processor?

Payments are woven into every part of your club. Memberships, court fees, drop-ins, retail sales, event registration — the money flows from every direction. And if you’re relying on spreadsheets, disconnected tools, or crossed fingers to manage it all, something’s bound to slip through the cracks.

So, stop and ask yourself: how efficient is your current payment process — and how much is it costing you in time, errors, and manual work?

Consider all the moving pieces you’re managing for a moment:

Recurring memberships – Monthly, quarterly, or annual dues that need to be charged on time, every time.

Court reservations – Whether scheduled in advance or booked on the fly, these need to be paid for and confirmed without delay.

Clinics, private lessons, and drop-ins – With dozens of sign-ups and no-shows to manage, automation is key.

Retail or pro shop sales – From paddles and grips to apparel, you need to process quick, secure in-person payments.

Tournament fees or event registrations – These payments often come in waves, and you need a reliable system to handle them without errors.

Trying to manage all this manually — or across patchwork systems — inevitably leads to mistakes, missed payments, and unnecessary admin work.

When payments are coming in from all angles, you need more than a way to just accept money. You need a system that’s built for how tennis and pickleball clubs actually operate.

That’s what an integrated payment processor delivers: one place to handle it all — with less stress, fewer mistakes, and way more control. It simplifies how your club collects revenue across every program, product, and service you offer.

Why PayPal, Venmo, and Zelle don’t cut it for racquet club transactions

PayPal, Venmo, and Zelle are popular, familiar, and easy to use — and yes, they’re technically payment processors. That’s exactly why many racquet clubs turn to them as a payment solution early on.

However, there’s a big difference between processing a quick payment and managing the financial backbone of a tennis or pickleball club.

From limited features to usage restrictions, here’s why these platforms fall short for managing racquet club transactions:

1. Not designed for tennis or pickleball clubs

When you’re running a tennis or pickleball club, payments are just one part of the equation. You’re also managing memberships, scheduling courts, organizing events, and keeping programs running smoothly — often all at once. So, you need a payment solution that supports those daily operational demands and works in sync with your club management system.

That means:

Recurring billing for memberships, court reservations, lesson sign-ups, event fees, and retail sales

Integrated payments that link to court reservations, registrations, events, etc.

Real-time visibility into who paid, for what, and when

Generic payment tools weren’t built with any of that in mind. Even with their limited business features, they operate as standalone tools — not as part of your club’s ecosystem. That disconnect forces you to piece together workarounds, adding unnecessary steps, friction, and risk.

2. Limited features and customization

These platforms offer limited tools beyond basic payment processing. They don’t connect to court reservations, lesson sign-ups, or member accounts — so clubs are left managing payments separately from operations.

They also offer little to no automation or customization capabilities. That means more time spent juggling tools and manually tracking down payments — instead of focusing on your programs, players, and growth.

3. Higher fees for business transactions

While personal transactions may be free, business-related payments on platforms like PayPal and Venmo often come with higher transaction fees. And when you’re processing payments for dozens of memberships, clinics, or events each week, those fees can quietly chip away at your revenue. Worse, there’s no way to offset these charges as these platforms don’t allow you to pass fees on to players.

However, integrated processors like Stripe and SafeSave offer more flexibility and transparency — including the option to pass fees to players if you choose. That gives racquet clubs a way to preserve revenue and manage costs more strategically. Some even offer revenue-sharing opportunities, turning payment processing into a source of income instead of just a cost.

Every solution has its own fee structure, so it pays to do your research and read the fine print — especially when it comes to business use.

4. Potential violations of terms of use

Using these platforms outside their intended scope can result in suspended access or frozen funds.

Zelle prohibits using personal accounts for business payments unless enrolled through a bank’s small business offering.

Venmo doesn’t allow business transactions on personal accounts — violations may lead to account restrictions or closure.

PayPal enforces strict compliance policies for business activity, and misclassifying transactions can lead to account reviews or holds.

5. Cannot support high-volume operations

These payment platforms aren’t built for high-volume, multi-stream, or multi-location operations like those at racquet clubs. For instance, PayPal may impose holds or limits as your transaction volume grows. Venmo’s business profiles are designed for low-volume sellers and include weekly caps. Zelle’s business functionality depends entirely on your bank, with no centralized support or features.

Clubs handling frequent payments need tools designed to scale with their operations — not platforms that max out when things get busy.

While PayPal, Venmo, and Zelle are convenient for personal payments, they lack the functionality needed for managing complex club operations. Racquet clubs need more than just a way to collect payments — they need a purpose-built platform that seamlessly integrates with their players, programs, and systems.

Benefits of using an integrated payment processor at your tennis or pickleball club

Switching to a business-grade, integrated payment processor like Stripe or SafeSave isn’t just about getting money in the door — it’s a strategic move that improves every part of your club’s financial workflow.

From front desk to back office, here’s what the right solution can unlock:

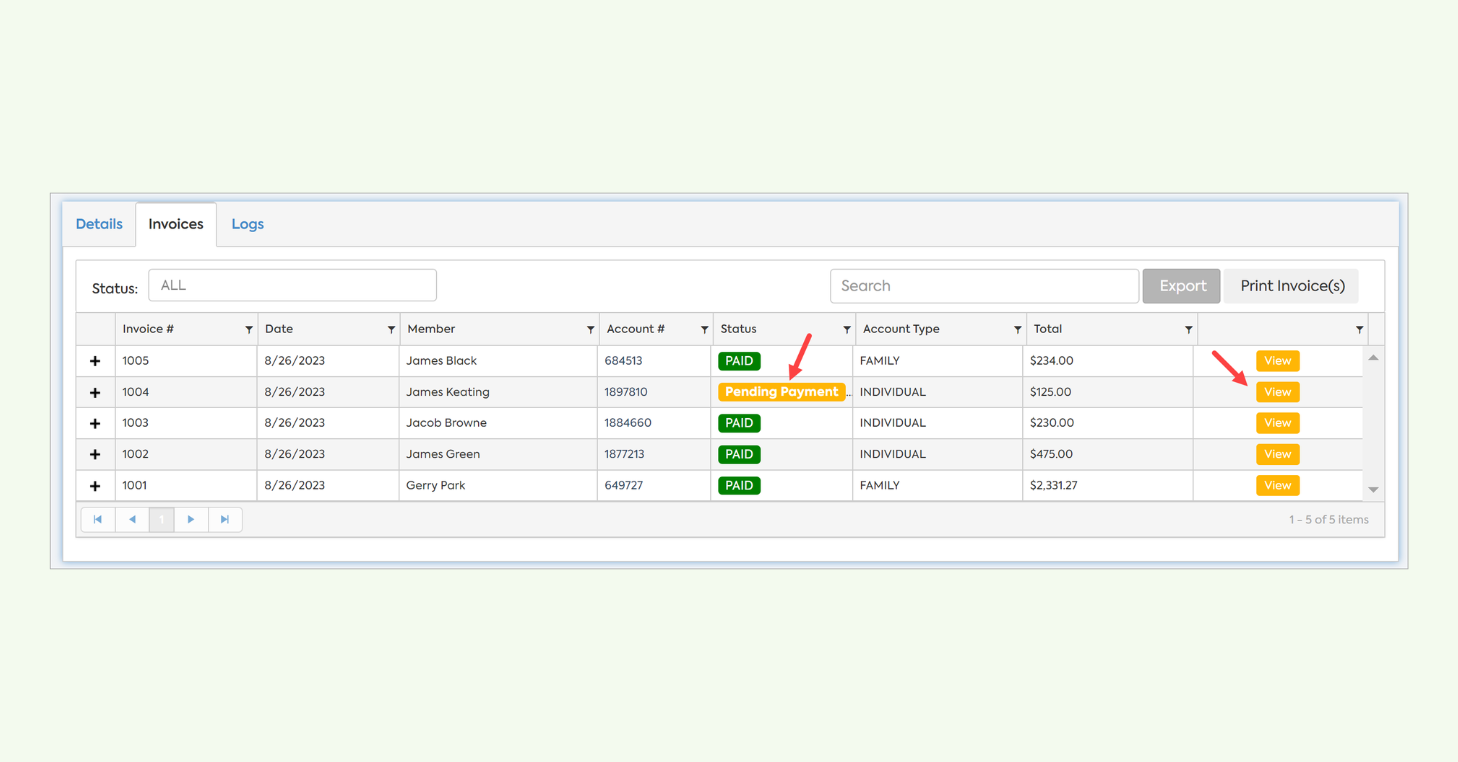

Example of invoicing capability within CourtReserve

1. Get paid on time, every time

Say goodbye to missed payments or awkward collection conversations. With common payment processor features like recurring billing, automated charges, and saved payment methods, players can set it and forget it — while your club gets paid on time, every time.

2. Reduce admin overload

Manual entry invites mistakes and wastes time. A payment processor automates routine tasks like invoicing, payment tracking, and account updates — freeing your staff to focus on running programs, not chasing receipts.

3. Provide member-friendly payment options

Players expect flexible, secure ways to pay — credit cards, ACH transfers, digital wallets, even stored payment options. Offering these builds trust and reduces friction during checkouts, bookings, and registrations.

4. Easily track all club income

A centralized system means no more compiling spreadsheets at year-end. Transactions are tracked, organized, and exportable — so your financial reports stay accurate and up to date.

5. Make payments safer for your club and players

With a PCI-compliant processor, you don’t have to worry about storing card details or meeting security standards on your own. Built-in encryption and fraud protection help keep both your club and your players safe.

Video Transcript

(0:00) Hello everyone. It’s Ashley with Court

(0:02) Reserve. We are so excited to have you

(0:05) on our call today. Uh we’re going to get

(0:08) started in just a minute, but just a

(0:10) couple of announcements. Uh of course,

(0:13) you know, we’re always trying to to be

(0:16) in areas where we think it’s uh relevant

(0:19) for our clubs and things. And so, we’re

(0:21) going to be heading out on the city

(0:23) series tour with the Rackadex uh club

(0:26) series. Uh we’re going to Philadelphia

(0:28) next weekend. super excited. Uh if you

(0:30) actually get on our Instagram or

(0:32) Facebook page, we’re we’re going to be

(0:33) giving away some free tickets to this,

(0:36) but you got to be on Instagram and

(0:37) Facebook. So, join that and you’ll see

(0:40) uh how you can do that as well. And then

(0:42) if it’s not too late, we’re doing

(0:44) mastermind. It actually starts tomorrow.

(0:47) Might be a little late this time, but if

(0:48) you’re a pickle ball facility in any

(0:50) manner, we highly recommend you

(0:52) eventually go to mastermind. You’re

(0:54) going to you’re going to spend money

(0:55) somehow. Might as well not waste it. Go

(0:57) to mastermind. We highly recommend it.

(0:58) Our team’s out there in Utah this week

(1:01) uh with our pickle ball folks. And then

(1:04) if you are here and you’re a court

(1:06) reserve user, you got to come to a

(1:07) catalyst. We have put so much just this

(1:11) year into court reserve and just wait

(1:13) till you find out what we’re going to

(1:15) release on July 9th. Um I’m not putting

(1:17) I’m not giving any uh clues, but

(1:20) definitely get your tickets. We’re going

(1:21) to Seattle, Washington September 15th

(1:24) and Skiilman, New Jersey, right outside

(1:26) of Cherry Hill September the 30th. So,

(1:28) we are super excited about that as well.

(1:31) So, today, regardless if you use Safe

(1:34) Save payments or not, there’s a couple

(1:37) others. There’s Stripe, there’s some

(1:38) other folks. You are going to learn so

(1:40) much today about chargebacks. These are

(1:43) experts at Safe Save. Rachel and Shane,

(1:46) welcome uh to the court reserve webinar

(1:48) series. We are so happy to have you guys

(1:50) here today. Thanks for having us.

(1:53) Absolutely. So, um, if you’re a business

(1:56) owner, uh, you know, Tim and I, we

(1:57) opened up Old Coast, uh, pickle ball

(1:59) last April, and even Court Reserve

(2:02) itself, we occasionally have had people

(2:05) come in and say, “Oh, no. I I don’t want

(2:07) to pay for this. I’m I’m charging back.”

(2:09) So, Rachel, first of all, tell us what a

(2:12) chargeback is. So, a chargeback is

(2:15) basically when a customer goes directly

(2:17) to their bank to dispute a charge uh

(2:20) rather than speaking to the merchant.

(2:23) Nowadays, that’s often just a button in

(2:26) their banking app. So, it makes it easy,

(2:28) sometimes a little too easy, to skip you

(2:31) entirely and get a refund. Yep. So, they

(2:33) don’t even go back to the business. They

(2:35) don’t even call us at Old Coast Pickle

(2:36) Ball and say, “Hey, I want to talk to

(2:38) you about this charge.” They just go

(2:39) right back to the cart or right back to

(2:40) the bank. Yep. It’s It’s a dirty

(2:43) practice. Yes. All right. And so I know

(2:46) you have a slideshow uh ready to go for

(2:48) us. I’m super excited. So why don’t you

(2:51) just go ahead, you and Shane, just take

(2:52) it over and and you guys, I know you’re

(2:54) going to have questions. Put them in the

(2:57) um let’s see, do we want to put them in

(2:58) the chat or the Q&A? I actually like the

(3:00) Q&A better. Uh so if you’ll put your

(3:03) questions today in the Q&A, uh we’ll go

(3:05) through those as we go ahead. So Rachel

(3:07) and Shane, take it away. Thanks. Just

(3:11) pulling up my notes. So, welcome to

(3:13) today’s session on chargebacks. Um, I’m

(3:16) I know they’re a hot topic right now out

(3:18) there in the payment processing world.

(3:21) Um, the objectives of today’s session is

(3:24) to have you all understand chargebacks

(3:27) at a higher level. Um, prevent them

(3:29) before they start whenever possible.

(3:31) Sometimes that’s unavoidable, but every

(3:34) time we can, we will. um respond

(3:37) effectively when you do receive a charge

(3:38) back and reduce your overall fraud risk.

(3:41) Um so in 2023, the average card holder

(3:44) filed almost six chargebacks each um at

(3:47) around $76 a chargeback. Um so that was

(3:51) $65.2 billion in chargeback disputes in

(3:55) 2023 and that number has gone up

(3:57) significantly since then. Um and it is

(4:00) expected to continue to rise

(4:01) unfortunately.

(4:03) Um, let me hit the next.

(4:08) Um,

(4:10) so what is a chargeback? We went over

(4:12) this briefly, but a little more detail.

(4:14) Um, a chargeback is a forced reversal of

(4:16) funds, a forced refund directly from the

(4:19) bank. it skips the merchant, skips the

(4:21) payment processor entirely and starts a

(4:24) process at the banking level to

(4:29) ultimately often recoup those funds for

(4:31) the customer. Um, it was created as part

(4:35) of a federal act to protect consumers um

(4:38) from fraud, billing errors, etc. Um, and

(4:41) it has expanded into a much larger issue

(4:45) for merchants, consumers, everyone

(4:47) involved. Um it is different because

(4:50) merchants have no control over the

(4:52) initiation or outcome of this refund. Um

(4:55) and it does cost you money and time even

(4:57) when you do win. Um chargeback volume is

(5:01) expected to grow almost 25% over the

(5:04) next three years. Um reaching almost 330

(5:08) million chargebacks annually.

(5:13) [Music]

(5:15) Uh so who’s involved? There’s many

(5:18) parties. Um, so ultimately the card

(5:21) holder, whether that’s the customer or

(5:24) if your customer used someone else’s

(5:26) card, the true card holder, um, the

(5:29) issuing bank, uh, the card network. So,

(5:32) Visa, Mastercard, Discover, American

(5:34) Express, they control the rules for

(5:37) compelling evidence, for timelines, for

(5:40) the processing of disputes.

(5:42) um they are really the backbone of the

(5:45) entire process. Um your payment

(5:48) processor. So in our case that’s safe.

(5:51) We act as the middleman for the process

(5:54) rather than controlling anything. We

(5:56) really h advocate for our clients in the

(5:58) process. Help submit documentation and

(6:01) notify you when a chargeback is filed.

(6:05) Um and then of course there’s you as the

(6:07) merchant. And I do have a timeline. Cute

(6:10) little photo here. Um, so you can see

(6:13) just how complex this process can be.

(6:16) Um, so it starts with the card holder

(6:18) and it goes through all three separate

(6:20) parties to reach you as the merchant.

(6:22) After you receive the chargeback, if you

(6:24) do choose to dispute, you communicate

(6:26) that to your merchant services provider.

(6:29) We communicate it usually through a

(6:31) portal to the card network. card network

(6:34) communicates with the issuing bank and

(6:36) then the dispute process and the review

(6:38) of evidence occurs to come to a

(6:40) resolution.

(6:44) So here’s that same timeline written out

(6:46) for all of you verbal folks. Um so

(6:52) with SAFE save you have seven days to

(6:54) respond. Dispute timelines vary based on

(6:57) payment processor. Um it’s typically

(7:00) between 5 and 20 days, but the

(7:03) resolution is required by law to um

(7:06) occur within 90 days. We almost never

(7:10) see it go beyond 90 days and often

(7:12) closer to the 30-day mark. If you win,

(7:15) your funds are returned. Um if you lose,

(7:18) the transaction stands and the customer

(7:20) is refunded. Um but no action, ignoring

(7:24) the notice is an automatic loss of those

(7:26) funds for you guys.

(7:29) Um and some common chargeback reasons.

(7:34) Um some things you’ll hear from

(7:36) customers and we hear through the

(7:38) process is customers go to their banks

(7:40) and say they didn’t authorize the charge

(7:42) that they were cancelled. They cancelled

(7:44) and were still build. Oftent times this

(7:46) is uh after they have gone beyond your

(7:52) cancellation policy. So they want a

(7:54) refund and have not been provided this

(7:56) refund. um they never received the

(7:58) service. So in for tennis clubs, pickle

(8:01) ball clubs, that’s often for rain dates

(8:03) and things where an account is being

(8:05) credited. Um they don’t recognize the

(8:07) charge or system errors, unclear

(8:10) policies, things that um are typically

(8:13) resolved with communication. So I have a

(8:16) question, Rachel. So are for you guys at

(8:20) Safe Save, this is kind of, you know,

(8:22) going through that, but are most payment

(8:25) processors doing the same kind of thing

(8:27) or or are these things that you guys do

(8:30) specially because like you’re fantastic

(8:32) people like tell us a little bit about

(8:33) that. Is this a normal process for all

(8:36) payment providers?

(8:38) So it is to an extent. So the difference

(8:41) with Safe Saves is that we are a much

(8:43) smaller team. So, when you email or are

(8:45) getting a chargeback notice, you’re

(8:47) getting it from me um or my teammate. Uh

(8:52) so, when you reply with a dispute or a

(8:53) question, rather than a robot or going

(8:56) through an automated system, there’s a

(8:58) real person on the other end going

(9:00) through your documents with you, looking

(9:01) at the dispute information, and trying

(9:03) to help you navigate that system. Um

(9:06) many other payment processors are a

(9:09) larger group of people. Um, so you don’t

(9:11) necessarily get the same amount of help

(9:13) or personal attention. Um, but the

(9:16) general flow of things from card holder

(9:19) to bank to merchant services provider is

(9:23) the same. Just awesome. Just to piggy

(9:25) back um on Rachel’s point there. So the

(9:27) universal chargeback process as a whole

(9:29) is the same. The steps it goes through,

(9:31) the bank, the card brands, etc. Well,

(9:34) we’re different and like Rachel said,

(9:35) we’re a smaller team. So we’re sending

(9:36) you an email notice almost right away.

(9:38) Other processors we’ve worked with send

(9:40) out a letter via snail mail, which could

(9:42) take a week or two to get to you. So now

(9:44) your timeline to respond is even

(9:45) shorter. You’re probably dealing with an

(9:47) automated system robot as Rachel

(9:49) mentioned. Um, so that’s just one way

(9:51) we’re different, but the steps it goes

(9:54) through behind the scenes through Visa,

(9:56) Mastercard, all of that is the same. Uh,

(9:58) but our methods for notification are are

(10:01) a lot quicker. That’s awesome. Thank you

(10:03) guys. Yeah, thank you. Um,

(10:07) so every time you receive a chargeback,

(10:10) the first question, and honestly, the

(10:13) main question you should be asking is,

(10:15) should you respond to the chargeback?

(10:18) Um,

(10:19) to do that, you should really do a

(10:21) costbenefit analysis and review the

(10:23) documentation you do have. So, can you

(10:26) prove the service was provided? Do you

(10:28) have any signed agreements, any check-in

(10:30) logs? Um, did you disclose a

(10:33) cancellation refund policy? Was that

(10:35) clearly handled? Sometimes accepting a

(10:38) chargeback is better. Um, but that’s on

(10:41) a case- by case basis. Say that a $5

(10:44) chargeback is going to cost you three

(10:45) hours of work.

(10:48) Your time is money. Um, you’re busy busy

(10:51) business owners. Your staff is busy. Um,

(10:54) is that $5 worth that three hours? And

(10:56) it’ll vary from business to business.

(10:59) Um, and you can always email uh uh if

(11:03) you use Safe Save, you can reach out to

(11:04) us and we can assist in figuring out

(11:07) what documentation is best or um there’s

(11:10) a lot of resources online as well as now

(11:12) in the court reserve uh knowledge base

(11:14) that can help with that as well.

(11:17) Um so if you do choose to respond,

(11:20) building a strong response is the main

(11:24) battle. Um so you want to be clear,

(11:26) common, factual. I try to explain it

(11:29) like you’re uh explaining the entire

(11:32) situation to a stranger. You want it to

(11:34) be clear, organized, complete. Um,

(11:37) jokingly I say it’s like you’re going on

(11:39) judge duty. You really have to make it

(11:41) easy to understand for the person on the

(11:44) other side who’s going to be reviewing

(11:46) all your documents. You have to connect

(11:48) all the dots with your evidence and your

(11:49) statement and directly dispute the

(11:51) chargeback reason that you’re given,

(11:53) which we can go into in the next slide.

(11:56) Um, so you can include booking policies,

(12:00) no-show conver confirmation, screenshots

(12:03) from court reserve are excellent. Um,

(12:06) signed policy agreements, attendance

(12:08) records, all of the above directly from

(12:11) Safe Save or your payment processor,

(12:13) including AVS, CVV, um, so that’s

(12:16) address verification. CVV is your

(12:19) security code on your card, like the pin

(12:20) on the back. Um, an IP address as

(12:23) evidence. Um, typically it’ll say if

(12:25) there was a match, a no match. You can

(12:27) look and see if the IP matches the

(12:29) billing location and that is strong

(12:31) supporting evidence as well, especially

(12:33) in fraud cases. Um, oh, and you

(12:36) definitely want to submit on time.

(12:37) Missing the deadline means that the card

(12:39) holder will win that case.

(12:43) Um, so some myths and misunderstandings.

(12:46) Uh, so this is like a true or false game

(12:49) going on. All chargebacks are fraud. Um

(12:53) it definitely feels that way but this is

(12:56) false. Um the chargeback system was set

(13:00) up to protect consumers and it does do

(13:03) its job in that way despite the new

(13:06) issue with friendly fraud. Uh safe and

(13:09) your payment processor can cancel a

(13:11) chargeback. Um we wish

(13:15) uh we cannot false. It is managed

(13:17) entirely by the card network um and the

(13:20) issuing bank. So, we have no ability to

(13:23) cancel or prevent a uh chargeback from

(13:26) being filed. I often wish I could for

(13:29) our clients, though. I will say um

(13:31) merchants can’t win disputes. Um the it

(13:36) feels this way for a lot of our clients

(13:38) that I speak to, especially after a big

(13:40) loss. But win rates can exceed 70% if

(13:43) you follow the rules and submit proper

(13:46) evidence. Um, evidence is the name of

(13:49) the game.

(13:51) Most chargebacks do stem from poor

(13:53) communication and criminal intent, not

(13:56) criminal intent. Um, I get a lot of

(13:58) emails saying exactly the opposite, but

(14:02) uh, it is true. Uh, chargebacks are

(14:05) often pure miscommunication, a lack of

(14:07) understanding from card holders.

(14:12) So, true fraud versus friendly fraud.

(14:15) This is huge right now in the chargeback

(14:18) world. Um, true fraud is everything we

(14:22) all think of when we think of fraud. So,

(14:24) stolen cards, identity theft, some bad

(14:26) actor on the other side trying to get a

(14:29) service for free or testing to see if a

(14:32) card works so they can use it elsewhere.

(14:34) Friendly fraud is what’s very become

(14:37) very common with chargebacks. Um, it’s

(14:39) also known as firstparty fraud, first

(14:42) party misuse. Um, but it’s typically a

(14:46) fraud claim or a chargeback that’s filed

(14:49) specifically uh to recoup funds. Maybe

(14:52) on accident because uh they forgot they

(14:55) purchased it or there’s a

(14:57) miscommunication of the family, but

(14:59) occasionally also because they’re

(15:00) confused or they regret the purchase and

(15:03) want their money back without

(15:04) communication often um or user error.

(15:08) Um, I know I have done this myself as a

(15:11) consumer where I see a charge on my

(15:13) debit card or my credit card and I go, I

(15:16) don’t know who that is. And I

(15:17) immediately go to press the button like

(15:19) to mark it as fraud or dispute it and

(15:22) then I go back later like, I’m so sorry,

(15:25) I figured out what it was. Um, even when

(15:28) a consumer goes back to reverse a

(15:31) chargeback, it’s still going through to

(15:33) the merchant. They’re still incurring

(15:34) fees. They’re losing time. Um, and most

(15:37) customers are not aware of this.

(15:41) Um, so the best chargeback is the one

(15:44) you’d ever get. Um, it’s much cheaper to

(15:46) prevent chargebacks than to fight them.

(15:48) Um,

(15:50) chargebacks cost around 375 for each

(15:53) dollar lost directly. Um, and this

(15:55) because of time lost, processing fees,

(15:57) damage to accounts or reputation.

(16:01) Um, so we’ll go over some best

(16:03) practices. Um, these are good overall

(16:06) business practices and they build trust

(16:08) in your clients, but they also build a

(16:11) documentation trail and make it more

(16:14) clear to your customers um, how to

(16:16) cancel, how to request refunds um, and

(16:19) prevent confusion and friendly fraud

(16:21) situations. Um, so clear visible clear

(16:26) visible policies are your first line of

(16:28) defense. You want to use every customer

(16:30) touch point to communicate them. Um, you

(16:33) can also submit this all as evidence um

(16:35) of agreement in disputes and it

(16:38) increases your chance of winning. Um, so

(16:40) you want to display cancellation or

(16:42) refund policies at checkout. Uh, court

(16:44) reserve does have the ability to require

(16:46) digital agreement terms at checkout.

(16:48) I’ve seen I’m sure Ashley can speak more

(16:50) about that if anyone uh needs

(16:53) information on that. Um, and you do want

(16:55) to avoid ambiguous language. So rather

(16:58) than maybe refunded, you say refunds

(17:00) provided within this amount of time for

(17:03) if you so like can a refunds provided

(17:06) for cancellations within 24 hours,

(17:08) something like that. Um you got have to

(17:11) be very very clear. Um and I do have

(17:14) examples of that that are in the court

(17:16) reserve knowledge base or going into the

(17:18) court reserve knowledge base. Um you

(17:20) want to send confirmation emails with

(17:22) full booking details whenever you can.

(17:24) Um, and include information on how

(17:27) cancellations and refunds work in all

(17:30) communications. Uh, proactively remind

(17:32) your customers of their upcoming

(17:34) sessions. Document every cancellation

(17:36) and complaint in writing. When you

(17:38) document things in writing, you can

(17:40) submit that in the case that a dispute

(17:43) is filed, that a chargeback is filed.

(17:45) Respond quickly, keep detailed records,

(17:48) train your staff, contact members early.

(17:51) Um, yeah, I think that that covers many

(17:54) things and of course this will go on for

(17:57) ever with documentation options. Well,

(17:59) and I’d love to speak to that because in

(18:01) aside court reserve, there are a couple

(18:03) different places. Definitely, people can

(18:05) go in right now and on payment receipts,

(18:08) they can add additional notes, you know,

(18:10) that go along with. So, if you’re

(18:12) running a point of sale and you’re

(18:13) selling drinks or merchandise out of

(18:15) your point of sale shop, you could

(18:16) definitely have a refund policy on

(18:18) there. Um, you know, we also have the

(18:21) waiverss and liabilities within court

(18:22) reserve. So, you could always put your

(18:24) refund policies in the documentation

(18:27) when the member first joined your

(18:29) organization. Now, does anybody read

(18:31) that? No. But you can prove that they

(18:35) signed it when they joined your facility

(18:37) as well. Um, you can put refund policies

(18:40) on your member portal. U, there’s lots

(18:42) of different ways. And so what Rachel is

(18:45) describing is different ways that you

(18:48) can, you know, add these refund

(18:50) policies, what your procedures are. Of

(18:51) course, you can print them out, put them

(18:53) at your front desk, uh, put them on the

(18:55) app. Uh, but as well, I think it’s just

(18:58) good for you to even think about this

(19:01) because I was telling Rachel and Shane

(19:03) before this, you know, at Old Coast

(19:04) Pickle Ball, I don’t even know if we

(19:05) have this written anywhere. So, we want

(19:07) to make sure that we are presenting, you

(19:10) know, this is exactly how it is. this is

(19:12) our refund policy and etc. So I know

(19:15) that Rachel you’ve created four uh

(19:18) documents for us at court reserve

(19:20) specifically for safe clients and we are

(19:23) working on putting those documents into

(19:26) the court reserve knowledge base under

(19:27) those safe articles. Um so if you’re

(19:30) interested um in reading what those are,

(19:33) I know Rachel’s going to go over them,

(19:34) but just reach out to support later on

(19:36) and then we can show you where that

(19:38) lives. So cool. Thank you. Yeah, it’s uh

(19:42) good policies overall and great evidence

(19:46) to submit as well, although I hope you

(19:48) can avoid needing to submit.

(19:52) Um so using court reserve and safe save

(19:54) safe to prevent and respond. Um so court

(19:56) reserve has a lot of great features for

(19:59) managing your customers. Um tracking

(20:01) attendance and cancellations is huge. Um

(20:04) submitting that as evidence in dispute

(20:07) is also incredibly helpful. um card

(20:10) networks do take attendance seriously

(20:13) and proving that they attended either

(20:15) through the court reserve features of

(20:18) tracking or images. I’ve had people

(20:20) submit images from their security

(20:23) cameras even um it also logs check-ins

(20:26) messages. You can create custom forms

(20:28) and Ashley talked about um modifying

(20:31) where policies are placed on the website

(20:34) in the app um etc. uh safe we for

(20:39) prevention we do have real time fraud

(20:42) prevention solutions. Um so we have

(20:44) fraud prevention available in each

(20:45) gateway that can be managed by the

(20:49) merchant directly. Um you can also reach

(20:51) out to our customer service team if you

(20:53) want any help going through that and

(20:55) figuring out what works best for you.

(20:58) Oftent time this means uh modifying CVB

(21:01) or ABS settings. Um and we have some

(21:04) other options as well. Um overall court

(21:08) reserve is incredibly secure. So card

(21:11) testing and other forms of fraud are a

(21:13) non-issue. However, uh preventing things

(21:17) like incorrect card use or using of

(21:20) someone using someone else’s card can be

(21:22) helpful with some of our settings in the

(21:25) gateway. Uh we’re also P PCI compliant

(21:28) so you don’t have to worry about data

(21:30) breaches um anything like that. you will

(21:34) get all of your dispute alerts via email

(21:36) and it has instructions on how to reach

(21:38) us for questions and submitting those

(21:40) disputes um and the support and guidance

(21:43) we offer. Um

(21:48) oh and uh this is just a fun fact. It is

(21:51) a marketing bonus to

(21:55) use the chargeback prevention tools and

(21:57) policies to build trust with your

(22:00) customers. Um, so by communicating

(22:03) clearly, having all of your policies

(22:05) posted, making it easy to understand how

(22:08) things are built and why they’re build,

(22:10) not only do you reduce disputes and

(22:12) chargebacks, but you improve your reput

(22:15) reputation. Um, members know you’re

(22:18) protecting their data, you’re practicing

(22:20) fair billing practices, um, and that

(22:22) you’re transparent and proactive in

(22:24) handling any concerns that do arise. Um,

(22:27) so it’s just a overall good uh business

(22:31) practice.

(22:34) Some fun real uh real world fraud

(22:37) trends. Um, so in a Forbes report on

(22:40) chargebacks, uh, merchants reported that

(22:44) at least 44% of chargebacks were

(22:46) friendly fraud. Other numbers that are

(22:48) not based on merchant reporting have

(22:50) this number even higher. Um, which is

(22:53) unfortunate. Um, fraud is not always

(22:56) what you think it is. It’s often a

(22:58) regular customer changing their mind or

(22:59) being confused. Um, so 84% of customers

(23:04) surveyed in the chargeback.io survey

(23:08) said filing chargebacks felt easier than

(23:10) requesting a refund. Um, a good

(23:13) prevention method is to try to make it

(23:16) easier to request a refund than to file

(23:18) a chargeback, which is the ongoing

(23:20) struggle. Um 72% of customers saw no

(23:25) real difference between filing a

(23:27) chargeback and requesting a refund and

(23:30) uh almost around half skip the merchant.

(23:33) Um

(23:35) uh card testing fraud is rising but it’s

(23:39) incredibly low when utilizing uh risk of

(23:43) sorry I have Wednesday brain. Uh there’s

(23:46) a really low risk of hard testing fraud

(23:48) utilizing court preserve because of

(23:49) login features and other security. Um

(23:54) so Rachel, what is surprising to me is

(23:57) that you know most people common people

(24:01) they don’t even realize what they’re

(24:03) doing when they do a chargeback. They’re

(24:05) actually hurting the business, right? No

(24:07) idea. And and they they just don’t know.

(24:09) And I mean it it’s interesting. I’m glad

(24:11) that we’re having this conversation

(24:12) today because this allows, like you

(24:15) said, for our clubs and facilities to

(24:17) really go above and beyond and and make

(24:20) sure that their policies are in place

(24:21) and that they can tell their players,

(24:23) hey, please come to us if you have a

(24:25) concern about a charge on your account

(24:27) and and maybe not have to go through the

(24:30) burden of all this chargeback stuff.

(24:33) Yeah, it’s a a game of prevention. And I

(24:36) do think that most customers if they

(24:38) knew the burden and the fees and

(24:40) everything associated with a dispute

(24:42) when they file it would not be filing

(24:44) them to begin with. We a lot of our

(24:46) customers are like our clients know

(24:49) their customers. They email in saying I

(24:51) know this person so well. I don’t

(24:53) understand why they’re filing this. Um

(24:55) and it’s often just a communication

(24:57) issue. So making everything very clear

(25:00) makes a huge difference. So good. Um

(25:03) yeah, and it’s uh

(25:06) just one note, chargebacks are popular

(25:08) right now because of the convenience of

(25:10) mobile apps and um all of that, but the

(25:14) lack of awareness, confusing return

(25:15) policies are a huge part of the

(25:19) increase.

(25:21) Um so preventing fraud without friction.

(25:24) So you like we talked about you want it

(25:25) to be everything to be clear. You want

(25:28) it to be so easy for your customers to

(25:30) go onto your website, go into the app

(25:31) and see who they have to talk to, who

(25:33) they have to email, who they have to

(25:34) call, can they press a button to request

(25:37) a refund, any of that. Um, so that they

(25:40) don’t have to go guess or search, press

(25:43) five clicks to find your policies. Um,

(25:47) enable the address verification system

(25:49) and CVB checks if you can. Um, you can

(25:53) work with our support team and call in

(25:56) and we can help you figure out what

(25:58) settings will work best based on your

(26:00) processing history. Um, and a lot of,

(26:03) uh, other payment processors will have a

(26:06) knowledge base or support team as well

(26:08) that you can work with. Um and requiring

(26:11) login for reservations is a um huge part

(26:16) of preventing card testing fraud as

(26:18) well, which is very much not an issue

(26:22) with court reserve, which is great. So

(26:25) Rachel, let me just stop you real quick.

(26:27) I just saw a question come in, so I

(26:29) figured we just answer this one real

(26:31) quick and give you a little breather. So

(26:34) um it’s asked that safe charges a $20

(26:37) non-refundable fee for chargebacks. Why

(26:40) is this fee not returned if we prove the

(26:42) chargeback is erroneous?

(26:45) So, the fine is my absolutely favorite

(26:48) part of chargebacks, and I’m sure Shane

(26:50) can agree. Uh, this is a fine that’s

(26:53) directly

(26:54) given to us as your payment processor by

(26:57) the card network and bank. Um, they say

(27:00) it’s for chargeback handling and

(27:02) processing. Um, but it’s not a safe

(27:06) making any money off of your

(27:08) chargebacks. being charged to us and we

(27:11) pass that to you as our client. Um, we

(27:15) do work with clients as best we can, but

(27:18) it’s overall um, something that is an

(27:21) unfortunate and standard practice in the

(27:23) chargeback world because banks are

(27:25) issuing this to all payment processors.

(27:28) So, so yeah, one thing we see with

(27:30) others is they’ll charge a monthly fee

(27:32) for chargeback handling. Whether you

(27:34) have them or not, you’re getting charged

(27:35) a $20 fee, a $30 fee. Not everyone does

(27:38) this. Most do, you know, how we do it is

(27:41) per occurrence. And as Rachel mentioned,

(27:43) we’re passing along what we’re charged.

(27:45) We’re not increasing that or upcharging

(27:48) it. But even if you win, that fee still

(27:50) sticks. Um it’s not like it goes away

(27:52) and we get refunded the fee. It it still

(27:54) applies regardless. Um the beauty

(27:58) business owner.

(28:01) Yeah. It’s very fun. Uh, I’ve also seen

(28:03) I I like to look at how other businesses

(28:06) are managing chargebacks as part of my

(28:08) job. Um, and I’ve seen some companies

(28:11) your first chargeback fine is free and

(28:13) then after that it’s $50 to $100

(28:15) depending on the uh case. Like there’s a

(28:19) lot of different ways of applying it,

(28:20) but the fee is uh standard unfortunately

(28:25) um and not charged to for fun or to make

(28:28) a profit. Let’s go. I’ve got a couple

(28:30) more questions here. Um, so one is let’s

(28:33) see, we would like our confirmation

(28:35) emails to provide more information to

(28:37) avoid issues. When will court reserve be

(28:39) building the ability to customize the

(28:40) confirmation and reminder emails? So

(28:43) currently you can go in and to those

(28:45) emails and you can add additional

(28:47) information, the payment receipt. Um,

(28:50) you can put it on your event

(28:51) registration emails, your lesson, and

(28:54) there’s a lot of stuff that you can do.

(28:56) Um, we are going to be working in Q3 to

(28:59) do more customization around emails, but

(29:02) right now you can certainly add

(29:04) additional information to those emails.

(29:06) Um, and so what I would do is if you

(29:09) have questions about how to do that,

(29:11) please reach out to support. Um, we’re

(29:12) definitely um, we can help you with

(29:14) that. And then the next question, if we

(29:17) get a chargeback request, decide that it

(29:20) is not worth contesting, so we refund

(29:23) the charge to the card. Does that fix

(29:26) the problem and avoid the fee?

(29:30) Unfortunately, no. Um I wish uh so when

(29:33) a chargeback is filed, it’s acting as

(29:35) the refund already. So, in all safe

(29:38) chargeback notifications, they’ll

(29:39) there’s a line saying to not attempt a

(29:41) refund in any way because the chargeback

(29:44) is the refund. Um, so if you want the

(29:47) card holder to receive a refund, you

(29:49) would either uh accept the refund

(29:51) usually via like for safe you reply

(29:54) saying accept or do nothing. Um, but you

(29:57) absolutely do not want to provide a

(29:59) refund on top of a chargeback. Um, as it

(30:02) then you will be out extra money and

(30:04) you’ll be in the negative. Um, so yeah,

(30:07) if you have questions, definitely reach

(30:08) out to Safe Save and support and and

(30:10) make sure that you don’t double them for

(30:14) Yeah, you don’t want to give away free

(30:16) money like that. It’s already a painful

(30:18) process. So, Right. That’s exactly

(30:20) right. All right, we have some more

(30:21) questions coming in. This is great.

(30:23) Where can we find the confirmation email

(30:25) that was sent to the customer to support

(30:28) these chargebacks when disputing? So,

(30:31) I’m assuming Cindy, if you’re talking

(30:32) about court reserve, all emails, you can

(30:35) actually go into um and I tell you what,

(30:39) Cindy, what I’ll do is I’ll try and get

(30:41) support to kind of make you a screenshot

(30:43) of where you can go in and see where

(30:45) emails live that go out of court

(30:46) reserve. And then what about from you,

(30:48) Rachel? Do you guys have any emails that

(30:51) you send out with with information that

(30:53) can be helped in the dispute?

(30:55) uh we don’t send any emails directly to

(30:57) customers but in the gateway we do carry

(31:00) um all of the transaction data and I

(31:04) have found that submitting a screenshot

(31:06) of the entire transaction is incredibly

(31:10) helpful especially for uh fraud. Um you

(31:14) can also pull your transaction history.

(31:16) So, if someone’s claiming fraud and say

(31:18) they have 10 other reservations they’ve

(31:21) made and not disputed, submitting those

(31:24) other notis disputed transactions, the

(31:26) transactions with no chargebacks is

(31:29) really great evidence that no, this is

(31:31) not fraud, this is just a confused or

(31:34) angry customer. Um, something like that,

(31:37) right? Are you telling me that sometimes

(31:39) people just get upset and they just do

(31:41) chargebacks because

(31:43) um it’s rare, but it does happen. It’s

(31:46) not a fun practice. I have seen uh I

(31:50) would say once a week I get a reply that

(31:53) this customer is just mad we won’t

(31:55) refund her because she received the

(31:57) services. Um how do we prove that she

(32:00) received the services and this is not

(32:02) fraud? Um, so there can be a malicious

(32:06) aspect.

(32:08) Luckily, it’s not super common, but we

(32:10) we have all had experiences with someone

(32:13) who just wants to show you how angry

(32:15) they are. Yes. So, all right, we got

(32:18) another question. Is there a

(32:19) determination on how the CVV code will

(32:22) be used either by court reserve or safe

(32:25) to avoid people loading incorrect card

(32:27) numbers into their payment profile?

(32:31) Oh, we were uh Oh, Shane, if you want

(32:33) ahead. Uh we have been working with Port

(32:35) Reserve on this and I believe that

(32:37) feature is incoming, but Shane, I don’t

(32:40) know if you have any updates. In terms

(32:42) of storing a payment profile, you

(32:44) actually can’t store a CVV. So, it’s not

(32:48) used for that purpose. And by default,

(32:50) we’re not requiring a match on a

(32:53) transaction. Um just because of the same

(32:56) storage issue, you can’t actually store

(32:58) it. But if it is provided on a

(32:59) transaction, you’ll see the response

(33:01) like did it match or did it not match on

(33:04) our side in the transaction history. We

(33:06) have settings. You can certainly enable

(33:07) it so that it must match or a

(33:09) transaction will fail. We can set that

(33:11) by but by default it is not. But if it

(33:13) is provided, you see if it matched or

(33:15) not um under the transaction details in

(33:18) the gateway. Nice. Yeah, the CBVB for uh

(33:21) saved payment methods is uh more

(33:23) difficult because it’s uh federally

(33:26) illegal to store the security pin, the

(33:29) CVB. Um so it does make it more

(33:33) difficult um in terms of

(33:37) blocking transactions through the CVB

(33:39) method. Address verification is

(33:41) typically better, but that has pluses

(33:45) and minuses too depending on which

(33:47) settings you choose. So reaching out to

(33:48) safe is always a a good call when

(33:51) modifying those settings. Awesome. These

(33:54) are great questions. Uh but Rachel, I’m

(33:56) going to let you continue on. Yeah. Um

(33:59) so we’ve gone over this a few times. Uh

(34:01) oh, we went over pretty much all of this

(34:04) already. Let’s see. Logins. Yeah, sorry.

(34:06) I’m catching up. Um so spotting fraud

(34:09) early. So, in cases of true fraud, um,

(34:11) which are incredibly uncommon with court

(34:14) reserve, however, they do happen,

(34:17) unfortunately. Um, you have some red

(34:21) flags you can look out for. A lot of it

(34:22) is unfortunately a gut feeling based on

(34:25) people acting strangely. Um, so

(34:29) customers being rude and evasive when

(34:31) they’re adding a payment method or, uh,

(34:34) changing their card 10 times and each

(34:36) time it’s failing. I don’t know many

(34:39) people who have 10 different credit

(34:41) cards to attempt a transaction with. Um

(34:44) disputing the last minute like

(34:46) cancelling last minute often disputing

(34:50) um unfamiliar names or locations. If

(34:52) you’re based in Florida and someone

(34:55) books online um from Washington

(35:00) just like they could be traveling or it

(35:03) could be um something a little weirder.

(35:07) So, keeping an eye on your payment

(35:08) processing overall and who’s signing up

(35:11) and just being aware as best you can of

(35:14) what your transactions are is a good

(35:16) best practice. Um, and you are in

(35:19) control of who you accept as a customer.

(35:21) Um, if something’s suspicious to you,

(35:23) you can reach out to Safe Save, you can

(35:25) reach out to Court Reserve, um, and

(35:27) protect your business first and

(35:29) foremost.

(35:31) Um, and last page. Um so the final

(35:34) takeaways uh for protecting your club’s

(35:37) bottom line with chargebacks and fraud.

(35:39) Um understand the process. Chargebacks

(35:42) cost time, money, resources, reputation.

(35:46) Um know the flow of chargebacks. Know

(35:49) who’s involved in the process. Um have

(35:52) clear policies. Uh communicate

(35:56) proactively.

(35:57) Keep strong documentation.

(36:00) Respond quickly and confidently. Um,

(36:03) watch for warning signs and leverage

(36:05) your partners. Sport Reserve is

(36:07) excellent. They’re here to help you.

(36:08) We’re here to help you at Safe Save.

(36:10) Your payment processors have knowledge

(36:13) bases and support teams you can reach

(36:15) out to. Um, so don’t be afraid to reach

(36:17) out for help and use the systems to

(36:20) really tackle these issues. Yes,

(36:23) definitely. Because I can tell you, you

(36:26) know, at Court Reserve, we’ve been

(36:27) around over eight years now and

(36:28) occasionally, you know, we’ve had a

(36:31) player accidentally come in and they’ve

(36:33) subscribed to court reserve. Now, why

(36:35) they did that, I don’t know, but they

(36:37) did. And then instead of coming to court

(36:39) reserve and saying, “Hey, I don’t know

(36:40) why you charge me. It’s the chargeback.”

(36:42) So, we’ve actually worked with Rachel a

(36:44) couple times, you know, on this. And so,

(36:47) Rachel, I want to share the kind of the

(36:50) documents. Um, do you want me to share

(36:51) the screen? Um, yeah, that would be

(36:53) great. Okay. All right. So, I’m going to

(36:55) share these documents just because I

(36:57) want to kind of show you guys uh what’s

(37:00) what what the the team has come up with.

(37:02) And we’re going to actually take these

(37:04) and put these in the um safe articles

(37:08) within the court reserve knowledge base.

(37:10) Um that’s where all of our articles and

(37:12) videos and things are. So, one, they’ve

(37:14) done a chargeback prevention guide. Um,

(37:17) again, a lot of this stuff we’ve kind of

(37:18) gone over today, but just wanted to kind

(37:20) of show you guys um, you know, how to

(37:23) handle this. Um, a customer dispute call

(37:26) log template. This is great because then

(37:29) you can use this internally. Um, keep

(37:31) good records. That way when you’re

(37:33) working with Rachel, you can already

(37:34) show her um, and and the merchant, you

(37:37) know, what you guys have already done. A

(37:39) chargeback response template. So, this

(37:41) is great because you’ve already given us

(37:43) the language uh that could be used uh

(37:46) for this and then the you know just an

(37:49) overview of chargebacks, what to expect,

(37:51) timelines, how we work with Safe Save,

(37:54) all the Safe Save emails and phone

(37:56) numbers and support um and everything.

(37:59) And so, I just wanted to share that with

(38:00) you guys. If you would like copies of

(38:03) these before we get them in the

(38:06) knowledge base because literally Rachel

(38:07) sent these to me this morning and I’m

(38:08) like, “Oh, that is so gold.” Uh, reach

(38:11) out to court reserve support and say,

(38:13) “Hey, I was on the safe webinar today

(38:15) and Ashley said I could ask for those

(38:17) four documents and we will send those to

(38:19) you. They’re PDFs, so so they’re really

(38:21) good right now.” So, any final

(38:24) questions? Please go ahead and put those

(38:26) in the Q&A so we can make sure and

(38:27) answer those. Um, you know, Rachel and

(38:31) Shane, I think, you know, in this day

(38:32) and time, as much, you know, as we would

(38:35) love to think that, you know, there’s no

(38:37) fraud out there at all and that people

(38:39) aren’t going to do this, I mean, it’s

(38:40) just part of of running a business. And

(38:43) so, I just want to thank you guys today

(38:44) for taking the time out to come on, you

(38:46) know, regardless if you use Safe Save or

(38:48) not, whether you use Stripe or another

(38:50) card merchant provider, this is really

(38:52) good knowledge for all businesses to be

(38:54) aware of. So, um, and you know, at Court

(38:57) Reserve, we’re constantly working to try

(38:58) and make it easy for you. So, again, if

(39:02) you need help with knowing where that

(39:04) extra line item is on your confirmations

(39:07) or your payment receipts within court

(39:09) reserve, reach out to support. I will

(39:11) let them know that you guys are on the

(39:13) way to ask questions because we want to

(39:15) make sure that we help you set up these

(39:17) policies and procedures um in order to

(39:20) to do and and to run your business more

(39:22) efficiently. Uh, we got a question. I

(39:24) assume that when a chargeback goes

(39:26) through, there is no change in the court

(39:29) reserve payment history of that member.

(39:32) So what happens within that? Do you guys

(39:35) can you talk about that a little bit? It

(39:37) has been a little bit since I’ve had a

(39:40) screenshot come through. I know that in

(39:42) safe it uh shows as failed. So when a

(39:45) safe uh when a transaction comes through

(39:48) as a chargeback, it’ll ch it’ll show a

(39:51) chargeback line. It’ll show sale,

(39:53) settle, chargeback, and when that

(39:55) chargeback happens, it changes the

(39:57) transaction to failed. Um, so I would

(40:00) have to check with court reserve support

(40:02) on how it shows on the court reserve

(40:03) side. I unfortunately don’t have a

(40:04) system myself. Um, but we do get a lot

(40:07) of uh questions being like, oh, I

(40:09) thought this transaction failed. Um, it

(40:11) just changes to failed, so you can’t

(40:13) provide a secondary refund because that

(40:15) would not be fun. And I just made sure

(40:18) and that is correct. there’s no change

(40:20) in the court reserve payment history. Um

(40:23) we don’t actually get any notification

(40:25) in court reserve that a chargeback is

(40:27) done. Um and so that would answer that

(40:29) question right there for sure. So good

(40:31) question. Yeah. And we do have uh

(40:33) automated gateway emails that’ll go out

(40:35) and tell you when a chargeback’s filed.

(40:36) and then our chargeback dispute email

(40:39) that has all the instructions on what to

(40:41) do, who to talk to, um what your options

(40:44) are and everything like that that we

(40:46) send out as well to the primary gateway

(40:48) contact.

(40:50) Anything else you can think of? Oh,

(40:52) let’s see. He’s got one more question.

(40:54) Uh so, how do I settle the reports in

(40:56) court reserve to show a chargeback? That

(40:59) is a great question and what I would

(41:01) encourage you to do is reach out to

(41:02) customer support because I don’t know

(41:04) the answer to that. I’ll be quite

(41:05) honest. Um, so I’m trying to get the

(41:08) answer for you right now, but if you’ll

(41:10) reach out to uh support at court

(41:12) reserve, then definitely um we can help

(41:15) you know what to do with that. The next

(41:18) question is, does Court Reserve place

(41:19) the $20 chargeback fee on the customer

(41:22) account? No, we don’t know when a

(41:24) chargeback happens within court reserve.

(41:26) And so if you want to charge your

(41:29) customer for doing a charge back, then

(41:32) you’ll have to go in and and assign a

(41:34) miscellaneous fee of somehow on that

(41:37) customer or that member’s um you know

(41:39) account within court reserve. So I do

(41:42) suggest uh including in your policies if

(41:45) you will share the fee with your

(41:47) customers if they file a chargeback

(41:50) accidentally. Um, just so you can That’s

(41:53) another great idea actually. Yeah. To

(41:55) have in your policy. So if they

(41:57) accidentally hit the button they’re

(41:58) charging back, then they’re going to

(41:59) help you pay for all the processing fee

(42:01) of $20 for sure. So um, we got another

(42:04) question. Should I contact the customer

(42:06) once I’m aware of a chargeback or just

(42:08) go through the process? I always suggest

(42:12) contact contacting the customer if you

(42:14) have the time. Um, time, cost, benefit,

(42:16) analysis always. But um oftent times you

(42:20) can resolve things directly with a

(42:23) customer either through accepting a new

(42:24) payment method or they can call and uh

(42:28) cancel the chargeback with their bank um

(42:30) and then send you an email confirmation

(42:33) of that cancellation. Um, so it’s worth

(42:37) it in my opinion to reach out. Um, and

(42:39) if they don’t answer, please contact

(42:42) Safe Safe or your payment processor and

(42:45) I would say um, if you would like to

(42:47) dispute and not have that be a refund,

(42:49) we should plan out your documentations.

(42:53) I wish Tracy question Tracy. Yeah,

(42:56) Tracy, that fee is part of something

(42:58) that even Safe Safe’s not doing. It’s a

(43:00) part of the policy of the the provider

(43:02) at what Visa, Mastercard, Discover, all

(43:04) those all those fantastic people that we

(43:06) love. So that fee does not go away. So

(43:09) that’s where she’s talking about Tracy

(43:11) where you can make it as part of your

(43:12) policy that if you do have to do go

(43:14) through this chargeback dispute, then

(43:16) you can share that pain with the

(43:18) customer that’s actually trying to

(43:19) charge back. So completely up to you

(43:22) guys. Unfortunately, that fee happens at

(43:25) the time the chargeback is initiated. So

(43:27) if a customer clicks that button in

(43:28) their bank that says dispute and then go

(43:30) two minutes later go oo accident and

(43:33) call their bank and say never mind it

(43:35) already got initiated that $20 already

(43:37) hit. So it’s it’s immediate. Really?

(43:40) Yeah. That’s why that fee like even if

(43:41) they win the chargeback or the

(43:42) chargeback’s canceled, it was already

(43:44) initiated. That’s when the fee applies.

(43:45) That’s why it still applies even if the

(43:47) customer cancels it. Uh the card holder

(43:50) cancels it. Sorry. Um because it’s at

(43:52) the time of initiation. Oh, lovely.

(43:54) Yeah. Yeah. It’s a very fun fun process.

(43:58) That’s why we got we gotta So, here’s a

(44:00) great question. How do you come up with

(44:03) a great policy for refunds and

(44:06) chargebacks, right? I mean, I’m thinking

(44:07) off the top of my head, I mean,

(44:09) everybody’s all AI crazy right now. Chat

(44:11) GBT might have some great

(44:14) like chat GBT like, hey, we need a great

(44:16) refund cancellation chargeback policy

(44:19) for our pickle ball or tennis club. What

(44:21) can you give me? And then the other

(44:23) thing I would do is I’m sure

(44:25) statebystate regulations also flow into

(44:28) this which is why court reserve we don’t

(44:30) actually give anybody any waiverss or

(44:32) disclosures. You have to get those

(44:33) yourselves. Um I will put a plug out

(44:36) there for Rocket Lawyer. Uh when court

(44:37) reserve first got started before we had

(44:39) an attorney. Uh we actually use Rocket

(44:42) Lawyer for a lot of basic documentation

(44:44) and it’ll do it per state. So it I mean

(44:47) it’s not very expensive. Uh it’s just a

(44:50) monthly fee and you can cancel at any

(44:51) time, but you might want to go out use

(44:53) chat GBT first. Uh and you know, then

(44:56) maybe verify that with your own state.

(44:58) Um yeah, that’s a great point. Yeah, I

(45:02) was going to say chat GBT as a first

(45:03) thought, but yeah, online your state.

(45:05) There’s tons of great resources. The

(45:06) unfortunate truth is you can have the

(45:08) best most rockolid policy ever and still

(45:10) lose. Yep. It’s unfortunate. It

(45:12) definitely helps and definitely

(45:13) increases win rate. But it’s just

(45:14) important to know with this process as a

(45:16) whole,

(45:18) even with the best, you sometimes will

(45:20) still lose, right? Yeah, for sure. It’s

(45:22) a there’s a person on the other end in

(45:25) the card network who’s reviewing

(45:26) documentation and their ability to read

(45:29) and understand and uh choice to read and

(45:33) understand is uh you know, it it throws

(45:37) everything in a whirlwind. Um, it’s a

(45:40) bit of a roller coaster out there, but

(45:42) uh, it is a good call to review things

(45:44) with a lawyer.

6. Modernize how you collect payments

Digital receipts, professional checkout pages, and polished invoices show players that your club is organized, credible, and current. These small touches build trust and reinforce that you’re running a professional operation — not a patched-together system.

7. Integrate payments with your club management system

With an integrated platform like CourtReserve, payments are built into the way you already operate. Reservations trigger charges. Registrations track automatically. Purchases are logged instantly. It’s not just convenient — it’s how modern clubs eliminate errors and streamline operations.

Payments built for clubs that mean business

Today’s tennis and pickleball clubs need payment systems that are as smart, efficient, and scalable as the rest of their operation. That means ditching the DIY workarounds and upgrading to an integrated payment platform that’s built to handle it all — automatically.

Because when your payments are reliable, secure, and connected to everything else in your system, you save time, reduce risk, and serve your players better.